The so-called wind and solar ‘industries’ will last for as long as the subsidies keep flowing, and not one second more.

Every time the subsidy reins get tightened, the rent seekers howl, claiming that they need them to run for just that little bit longer. Notwithstanding repeatedly crowing about wind and solar already being cheaper than conventional power generation sources. It’s a grand and self-serving hypocrisy, of course.

Sometimes the curtain slips just enough to reveal our critical the subsidies are, when it comes to encouraging investors in the greatest government-back scam of all time.

Steven Hayward takes a look at a group of investors (read ‘rent-seekers’) who got cold feet because it just isn’t enough to be made from one particular project because of a requirement to add expensive batteries and unreliable wind and solar.

Not Enough “Green” in Green Energy?

Powerline

Steven Hayward

3 June 2021

The business page of the Wall Street Journal yesterday reported one of those minor stories that you might blow past if you don’t stop and ask yourself about curious missing details. Here’s the lede (with the significant bits of half-news in my boldface):

US Grid Seeks New Investors After EnCap Pulls Out

Wall Street Journal

Luis Garcia

1 June 2021

A short-lived deal by EnCap Investments illustrates the challenges that private-equity firms investing in clean energy can face, including reaching their return targets through such transactions.

US Grid Co., which focuses on natural gas-fired power plants, is seeking new investors after EnCap pulled out of its investment in the New York-based company late last year, said Jacob Worenklein, US Grid’s chief executive.

EnCap backed US Grid in 2019 to help it acquire gas-fired plants in large U.S. cities then add battery storage and other renewable-energy systems to reduce emissions. But EnCap soured on the deal once it determined that the plants that US Grid could potentially acquire and modify wouldn’t meet the firm’s return expectations, said EnCap Managing Partner Jim Hughes. He leads the firm’s clean-energy investments.

“We just never found opportunities that we felt represented a good risk-reward ratio,” Mr. Hughes said. “We ultimately decided to back away from that strategy.”

Wall Street Journal

Green energy is supposed to be all the rage among investors these days, but this item suggests that perhaps the rate of return is subpar. Just what is the expected rate of return for this and similar investment firms? The story doesn’t say, and the Journal reporters don’t seem interested in or able to find out.

It could be that the technology mix (storage for renewable power alongside gas backup plants) is too immature or uncertain, and with natural gas prices on the upswing right now the margins for gas-powered plants are being squeezed. On the other hand, the whole world of electricity investment is badly deranged by subsidies, renewable mandates, and other market distortions. I wouldn’t want to touch it either. Can you say “stranded assets”?

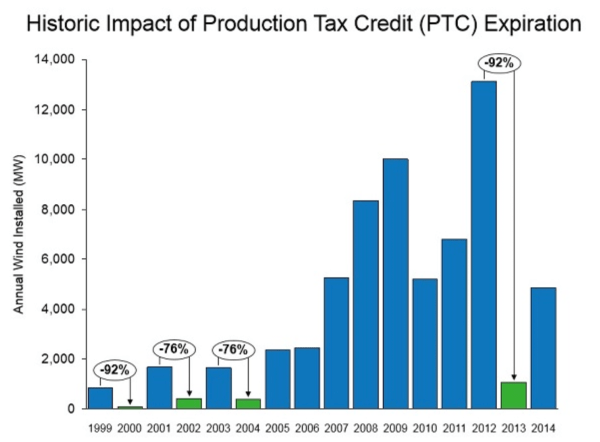

If you want to understand how subsidy-driven (meaning politically-driven) energy investment has become, check out what has happened to new wind power installations when the lavish production tax credit (PTC) for wind power has been allowed to expire several times over the last two decades: investors stop buying the things. No wonder the wind industry has fought (successfully alas) to extend the PTC for several years to come: it’s the only way they can guarantee a profit.

It doesn’t matter… what we want is subsidies, not electricity…