****

To call what South Australia’s Labor government has ‘gifted’ their constituents an energy ‘policy’, is to flatter it as involving some kind of genuine ‘design’. It’s an economic debacle, pure and simple.

The current mess started under former Premier, Mike Rann – a former spin-doctor, whose relatives lined up at the wind power subsidy trough from the get-go.

Under its current vapid leader, Jay Weatherill, SA’s Labor government has been talking up a wind powered future for months now – he’s presiding over the worst unemployment in the Nation, at 8.2% and rising fast – and seems to thinks the answer is out there somewhere – ‘blowin’ in the wind’. Its wind power debacle has led to South Australians paying the highest power costs in the Nation – if not (on a purchasing power parity basis) the highest in the world – and, yet, the dimwits that run it wonder why it’s an economic train wreck (see our posts here and here).

A few posts back – always ready to rain on the wind industry’s parade – as well as the gullible and corrupt that cheer it on – we spelt it out in pictures – that even the most intellectually interrupted should be able to grasp:

The Wind Power Fraud (in pictures): Part 1 – the South Australian Wind Farm Fiasco

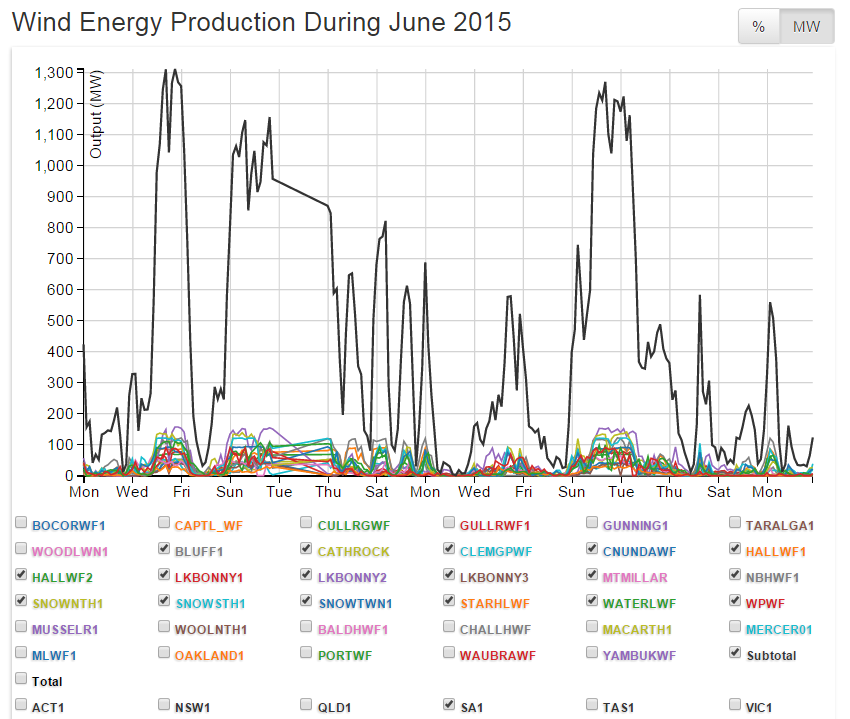

But that woeful missive merely drew focus on the pathetic performance of SA’s 17 wind farms; and their ‘notional’ installed capacity of 1,477MW – it has the greatest number of turbines per capita of all States – and the highest proportion of its generating capacity in wind power by a country mile.

Now, we’ll take a look at the effect on SA’s power market when wind-watts go completely AWOL, almost every other day. The chaos that wind power brings with it, has created the perfect opportunity for peaking power operators to make out like bandits at power consumers’ expense – simply because it can be predictably ‘relied’ on to disappear without warning.

Wind power driven, market chaos clearly has the Australian Energy Market Operator worried; as its ‘Pricing Event Report’ for July shows.

To make clear just what was driving rocketing spot prices, we’ve added pictures, care of Aneroid Energy.

And when we say ‘rocketing’ we mean with all the thrust of Apollo 11. For the year to date, SA’s average spot price for power is $72 per MWh (compared to Victoria’s $35) – the reason for the price difference might just come from the fact that the Victorians have a relatively tiny proportion of their generating capacity in wind power; and the largest coal-fired generators in the country.

Now, with SA’s average of $72 per MWh in mind, consider the number of occasions in July when – as wind power output collapses – the spot price approaches or hits the Market Price Cap. That cap – currently $13,800 per MWh – sets the upper limit of what peaking power generators can extort from the system: for a rundown on how the National Energy Market is designed to work, see this paper: AEMO Fact Sheet National Electricity Market

That’s the ‘design’; here’s the shocking reality.

Pricing Event Reports – July 2015

Electricity Pricing Event Report – Tuesday 28 July 2015 (TI ending 1830 hrs)

Market Outcomes: South Australian spot price reached $1,967.51/MWh for trading interval (TI) ending 1830 hrs.

South Australian FCAS prices (Volume Weighted FCAS Prices) and energy and FCAS prices for the other NEM regions were not affected by this event.

South Australia had an actual Lack of Reserve 1 (LOR1) from 1800 hrs to 2030 hrs (Market Notices 49437 and 49438).

Detailed Analysis: 5-Minute dispatch price reached $10,759.20/MWh for dispatch interval (DI) ending 1820 hrs. The high price can be attributed to rebidding of generation capacity and limited interconnector flows during the evening peak demand period. Wind generation was low during this period in South Australia.

The South Australian demand was 2,233 MW for TI ending 1830 hrs. During the same TI, wind generation in South Australia was at 18 MW.

For DI ending 1820 hrs, a total of 38 MW of generation capacity was rebid from Hallett PS and Northern PS unit 2 from bands priced at or below $590.07/MWh to bands priced above $13,333/MWh. South Australian generation capacity was offered at less than $591/MWh or above $10,759/MWh resulting in a steep supply curve.

Cheaper priced generation were restricted by their ramp rates (Mintaro GT) and FCAS profiles (Torrens Island A units 3 and 4). Generation offers at $10,759.20/MWh had to be cleared from Dry Creek GT unit 3 to meet the demand for the DI.

During the affected DI, the target flow towards South Australia on the Heywood interconnector was constrained to 403 MW by an outage constraint equation V::S_XKHTB1+2_MAXG. This transient stability constraint equation manages the Victoria to South Australia flow for the loss of the largest generation block in South Australia during the outage of both parallel Keith – Tailem Bend 132 kV lines.

The target flow on the Murraylink interconnector was limited to 68 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $104.27/MWh in the subsequent DI to the high priced interval when 673 MW of generation capacity was rebid from higher priced bands to the market floor price of -$1,000/MWh.

The high 30-minute spot price for South Australia was forecast in pre-dispatch schedules prior to TI ending 1130 hrs. The pre-dispatch schedule for TI ending 1830 hrs forecast a spot price of $590.07/MWh. The difference in prices between Pre-dispatch and Dispatch was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices.

Electricity Pricing Event Report – Tuesday 28 July 2015

Market Outcomes: South Australian spot price reached $2,390.06/MWh for trading interval (TI) ending 0800 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached the Market Price Cap (MPC) of $13,800/MWh in South Australia for dispatch interval (DI) ending 0750 hrs. The high price can be attributed to rebidding of generation capacity resulting in a steep supply curve during the morning peak demand period. Wind generation was low during this period in South Australia.

The South Australian demand was 1,915 MW for TI ending 0800 hrs. During the high priced TI, wind generation in South Australia was at 19 MW.

For DI ending 0750 hrs, AGL shifted a generation capacity of 160 MW from Torrens Island B PS from bands priced at or below $124.99/MWh to bands priced at MPC of $13,800/MWh. South Australian generation capacity was offered at less than $591/MWh or above $12,195/MWh resulting in a steep supply curve.

Cheaper priced generation were restricted by their ramp rates (Hallett PS, Mintaro GT, Quarantine PS unit 4) and fast-start profiles (Dry Creek GT unit 3) which required time to synchronise.

Generation offers at Market Price Cap (MPC) of $13,800/MWh had to be cleared from Torrens Island B PS to meet the demand for the DI.

During the affected DI, the target flow towards South Australia on the Heywood interconnector was constrained to 460 MW by the Victoria to South Australia Heywood upper transfer limit thermal constraint equation, V>S_460. The target flow on the Murraylink interconnector was limited to 61 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $109.32/MWh in the subsequent DI to the high priced interval when South Australia demand reduced by 77 MW. Approximately 101 MW of non-scheduled generation came online. Generation capacity was also rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

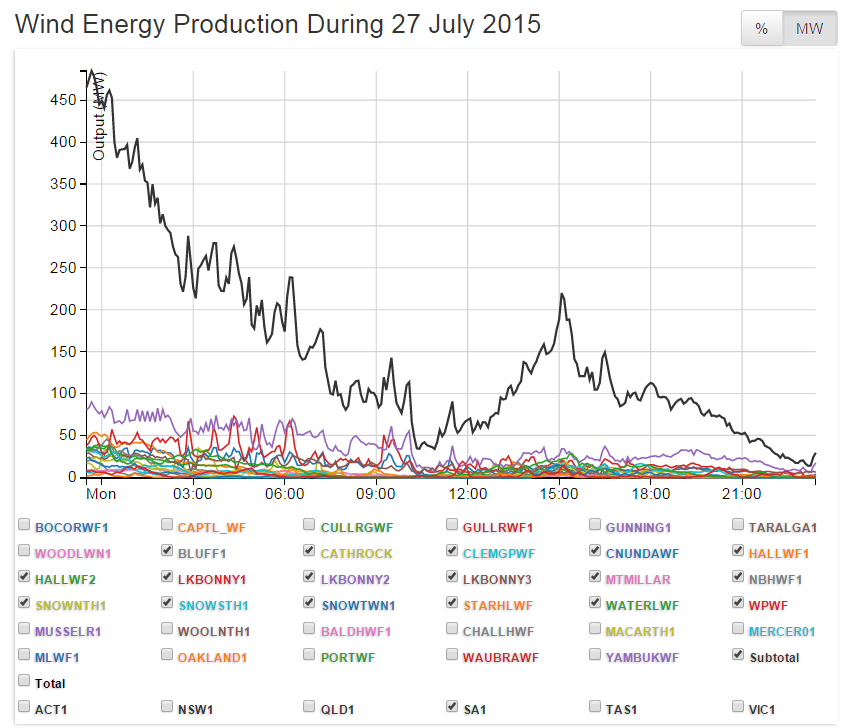

Electricity Pricing Event Report – Monday 27 July 2015

Market Outcomes: South Australian spot price reached $4,449.17/MWh for trading interval (TI) ending 0800 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached the Market Price Cap (MPC) of $13,800/MWh and $12,195.07/MWh in South Australia for dispatch intervals (DIs) ending 0755 hrs and 0800 hrs respectively.

The high prices can be attributed to rebidding of generation capacity resulting in a steep supply curve during the morning peak demand period. Wind generation was moderately low during this period in South Australia.

The South Australian demand was 1,896 MW and the temperature in Adelaide was 4.9 °C for TI ending 0800 hrs. During the high priced TI, wind generation in South Australia was at 141 MW.

For DI ending 0755 hrs, AGL shifted a generation capacity of 200 MW from Torrens Island B PS from bands priced at or below $174.99/MWh to bands priced at MPC setting the high price. South Australian generation capacity was offered at less than $591/MWh or above $10,759/MWh resulting in a steep supply curve.

Cheaper priced generation were restricted by their ramp rates (Hallett PS), FCAS profiles (Northern PS unit 2) and fast-start profiles (Dry Creek GT units 2 and 3) which required time to synchronise.

For DI ending 0800 hrs, cheaper priced generation were restricted by fast-start profiles (Dry Creek GT units 2 and 3) which required time to synchronise. Generation offers at $12,195.07/MWh had to be cleared from Hallett PS to meet the demand for the DI.

During the high priced DIs, the target flow on the Heywood interconnector was limited up to 418 MW towards South Australia by the binding transient stability constraint equations, V::S_NIL_MAXG_SECP and V::S_NIL_MAXG_AUTO. The V::S_NIL_MAXG_SECP constraint equation prevents transient instability by limiting flow on the Heywood interconnector from Victoria to South Australia for the loss of the largest generator in South Australia for periods when the South East capacitor is unavailable for switching. The V::S_NIL_MAXG_AUTO constraint equation prevents transient instability by limiting flow on the Heywood interconnector from Victoria to South Australia for the loss of the largest generation block in South Australia.

The target flow on the Murraylink interconnector was limited to 58 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $174.99/MWh in the subsequent DI to the high priced interval when generation capacity from several South Australian generators were shifted to lower priced bands.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

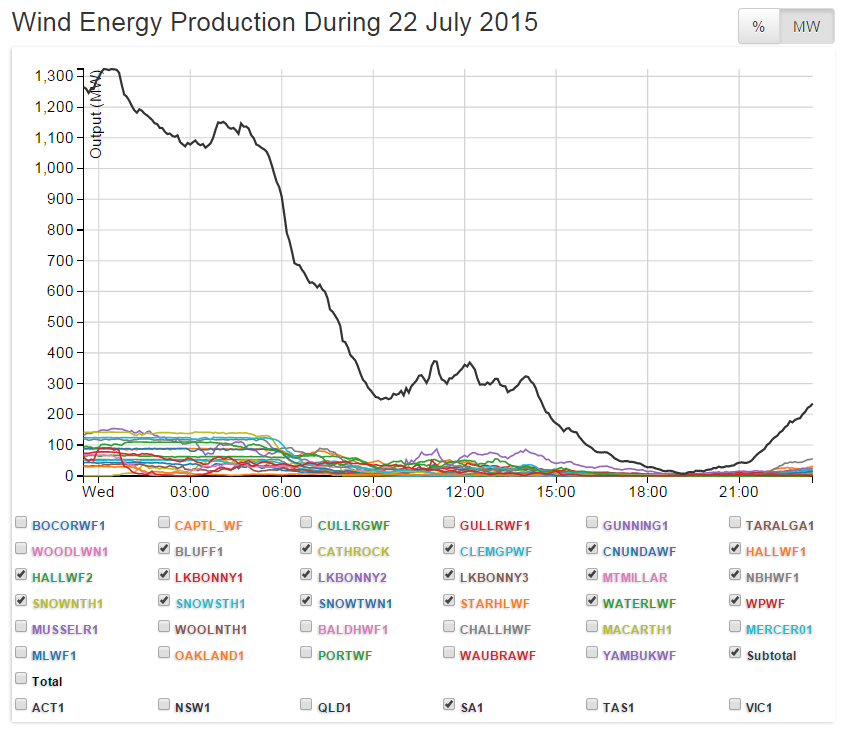

Electricity Pricing Event Report – Wednesday 22 July 2015

Market Outcomes: South Australian spot price reached $2,296.07/MWh for trading interval (TI) ending 1830 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached $13,481.81/MWh in South Australia for dispatch interval (DI) ending 1810 hrs. The high price can be attributed to a steep supply curve of generation capacity offered during evening peak demand period when wind generation was low in South Australia.

The South Australian demand was 2,100 MW for TI ending 1830 hrs. During the high priced TI, wind generation in South Australia was low at 39 MW.

For DI ending 1805 hrs, Energy Australia shifted a generation capacity of 34 MW from Hallett PS from bands priced at $360.81/MWh to bands priced at $13,481.81/MWh. For DI ending 1810 hrs, AGL rebid a generation capacity of 100 MW from Torrens Island B PS from bands priced at or less $64.99/MWh to bands priced at $13,500/MWh. South Australian generation capacity was offered at less than $591/MWh or above $10,750/MWh resulting in a steep supply curve. Cheaper priced generation was restricted by FCAS profiles (Northern PS unit 2 and Torrens Island PS unit A4) and fast-start units (Mintaro PS and Quarantine PS) which required time to synchronise.

Generation offers at $13,481.81/MWh had to be cleared from Hallett PS to meet the demand for the DI.

The target flow on the Heywood interconnector was limited to 447 MW towards South Australia by the binding transient stability constraint equation, V::S_NIL_MAXG_AUTO. This constraint equation prevents transient instability by limiting flow on the Heywood interconnector from Victoria to South Australia for the loss of the largest generation block in South Australia. The target flow on the Murraylink interconnector was limited to 64 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1.

This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $53.42/MWh in the subsequent DI to the high priced interval. South Australia demand reduced by 103 MW when 101 MW of non-scheduled generation came online. Generation capacity was also rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

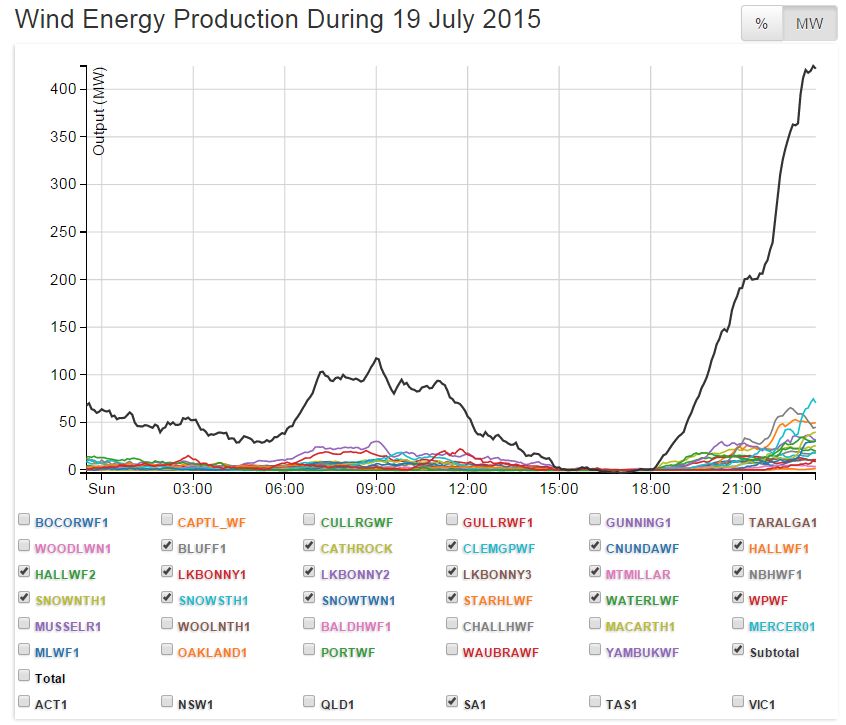

Electricity Pricing Event Report – Sunday 19 July 2015

Market Outcomes: South Australian spot price reached $2,372.11/MWh for trading interval (TI) ending 1830 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price in South Australia reached $13,333.95/MWh for dispatch interval (DI) ending 1830 hrs. The high price can be attributed to a steep supply curve in generation capacity during the evening peak demand period when wind generation was low in South Australia.

The South Australian demand was 2,066 MW for TI ending 1830 hrs. The high evening peak demand was due to the cool weather in Adelaide, with a low temperature of 7.3°C at 1830 hrs. During the high priced TI, wind generation in South Australia was low at 3 MW for TI ending 1830 hrs.

For DI ending 1825 hrs, Alinta Energy rebid 95 MW of Northern PS generation capacity from bands priced at or less than $286.95/MWh to $13,333.95/MWh. South Australian generation capacity was offered at less than $591/MWh or above $10,750/MWh resulting in a steep supply curve for the high priced DI. Cheaper priced generation were restricted by ramp rates (Torrens Island Unit A4), FCAS profiles (Northern PS Unit 2) or required time to synchronise (Hallett PS).

Generation offers at $13,333.95/MWh had to be cleared from Northern PS units to meet the demand for the DI.

The target flow on the Heywood interconnector was limited to 448 MW towards South Australia by the thermal constraint equation, V>S_NIL_HYTX_HYTX. This system normal thermal constraint equation manages post contingent flow on the Heywood 500/275 kV transformers by reducing Heywood interconnector flow when the actual flow exceeds the pre-defined transformer rating. The target flow on the Murraylink interconnector was limited to 64 MW towards South Australia by the outage constraint equation, V>X_NWCB6225+6021_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the North West Bend 132 kV circuit breakers from 13 July 2015.

The 5-minute price reduced to $115.77/MWh in the DI subsequent to the high priced interval when demand reduced by 111 MW and 101 MW of non-scheduled generation came online.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as the forecast demand in pre-dispatch was lower.

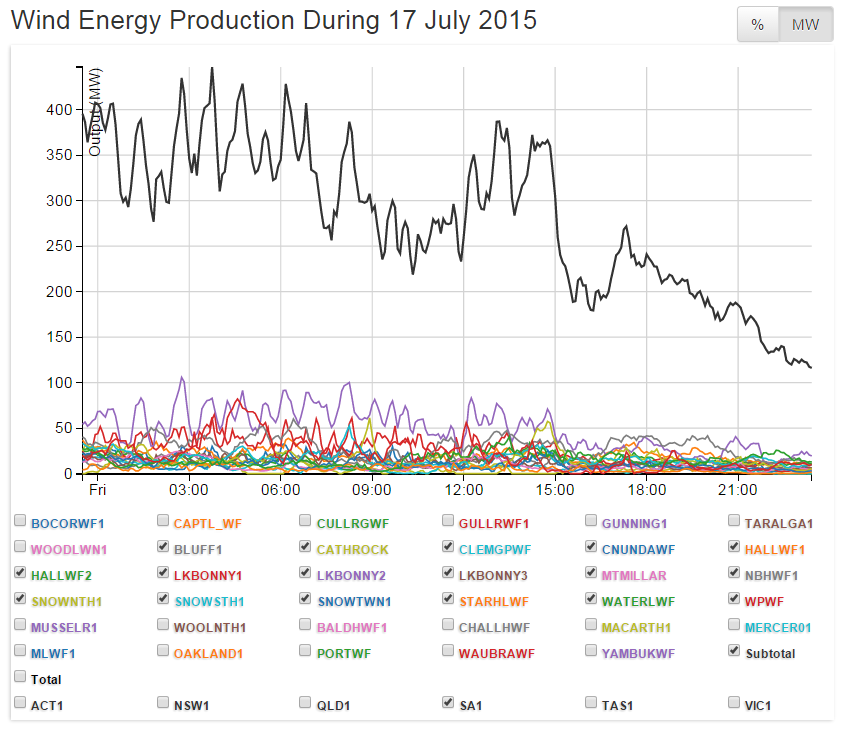

Electricity Pricing Event Report – Friday 17 July 2015 (TI ending 0000 hrs on 18 July 2015): South Australia

Market Outcomes: South Australian spot price reached $2,256.25/MWh for trading interval (TI) ending 0000 hrs (on Saturday, 18 July 2015).

FCAS prices and energy prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached $13,333.95/MWh in South Australia for dispatch interval (DI) ending 2340 hrs on 17 July 2015 during high demand period due to hot water load management (ripple control). Between DIs ending 2325 hrs and 2340 hrs, the South Australian demand increased by 311 MW. This additional load represented an 18% increase in the South Australian demand.

Wind generation in South Australia was approximately 120 MW for TI ending 0000 hrs on 18 July 2015.

At DI ending 2335 hrs, a total of 150 MW of generation capacity from Northern PS was shifted from bands priced at or less than $286.95/MWh to $13,333.95/MWh. The high price for DI ending 2340 hrs was set by Northern PS at $13,333.95/MWh. Cheaper priced generation was available from fast-start units (Hallet and Dry Creek unit 3) which required time to synchronise.

The target flow on the Heywood interconnector was limited to 449 MW towards South Australia by a thermal constraint equation, V>S_NIL_HYTX_HYTX for DI ending 2340 hrs. This system normal constraint equation manages post contingent flow on the Heywood 275/500 kV transformers by reducing the Heywood interconnector flow when the actual flow exceeds the pre-defined transformer rating. The target flow on the Murraylink interconnector was limited to 66 MW towards South Australia by an outage constraint equation, V>X_NWCB6225+6021_T1. This constraint equation manages limits flow from Victoria to South Australia on Murraylink during the planned outage of the North West Bend 132 kV circuit breakers from 13 July 2015.

The 5-minute price reduced to $47.13/MWh for the next interval (DI ending 2345 hrs) when the demand reduced by approximately 122 MW and 102 MW of non-scheduled generation came online. A total of 349 MW of generation capacity was also rebid from higher priced bands to the market floor price of -$1,000/MWh.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of a 5-minute load increase that caused a price spike in the 5-minute dispatch prices.

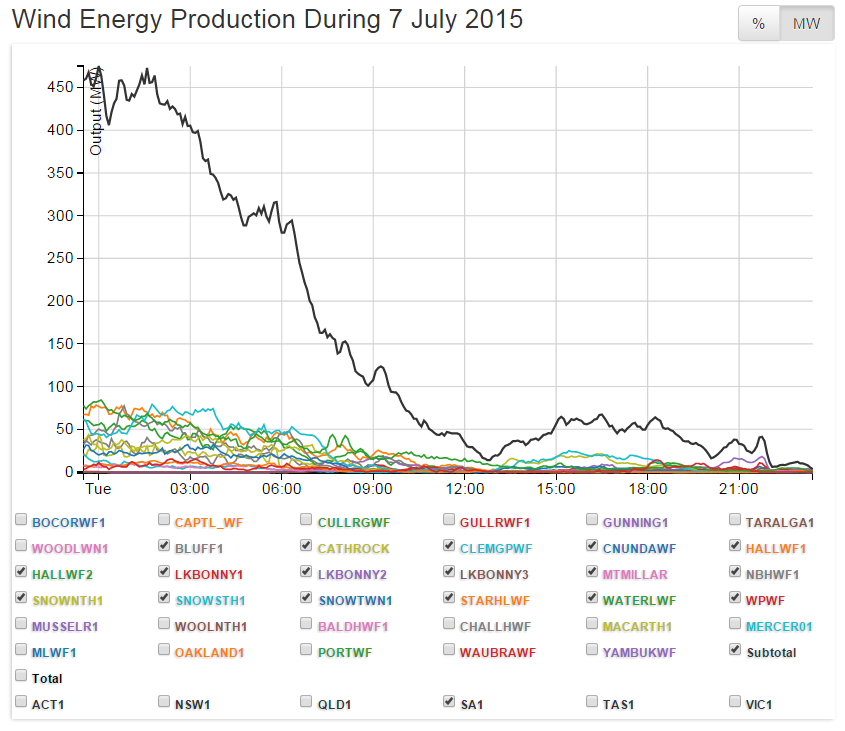

Electricity Pricing Event Summary – Tuesday 7 July 2015*

Market Outcomes: South Australia spot price reached $1,221.54/MWh for trading interval (TI) ending 1900 hrs. South Australia FCAS prices and energy and FCAS prices in other regions were not affected.

Summary:

South Australia 5-Minute dispatch price reached $6,794.04/MWh for dispatch interval (DI) ending 1855 hrs due to a steep supply curve in generation capacity during a period of low wind generation. Planned outages affecting the interconnector flow into South Australia also contributed to the high price.

- Low levels of wind generation in South Australia at approximately 60 MW at TI ending 1900 hrs

- Rebidding of 20 MW of Hallett PS generation capacity from bands priced at or less than $360.81/MWh to bands priced at $13,481.81/MWh for DI ending 1840 hrs

- For DI ending 1855 hrs, South Australian generation capacity was offered at less than $590/MWh or above $10,750/MWh resulting in a steep supply curve

- Cheaper priced generation were restricted by a fast-start unit (Dry Creek GT unit 3) which required time to synchronise

- The target flow on the Heywood interconnector was limited to 430 MW towards South Australia by a planned outage thermal constraint equation, V>S_APHY2_NIL_HYTX2. This constraint equation manages flow of the Heywood M2 transformer during the outage of APD-HYTS No. 2 500 kV line

- The target flow on the Murraylink interconnector was limited to 181 MW towards South Australia by a planned outage constraint equation, S>>RBTX1_RBTX2_WEWT. This constraint equation manages post contingent flow of Waterloo East – Waterloo 132 kV line for the trip of Robertstown No. 2 132/275 kV transformer during the outage of Robertstown No. 1 132/275 kV transformer.

South Australia energy price reduced to $46.14/MWh for DI ending 1900 hrs when:

- Demand reduced by 144 MW and 104 MW of non-scheduled generation came online

- Generation capacity was rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as the forecast demand in pre-dispatch was lower.

* A summary was prepared as the maximum daily spot price was between $500/MWh and $2,000/MWh

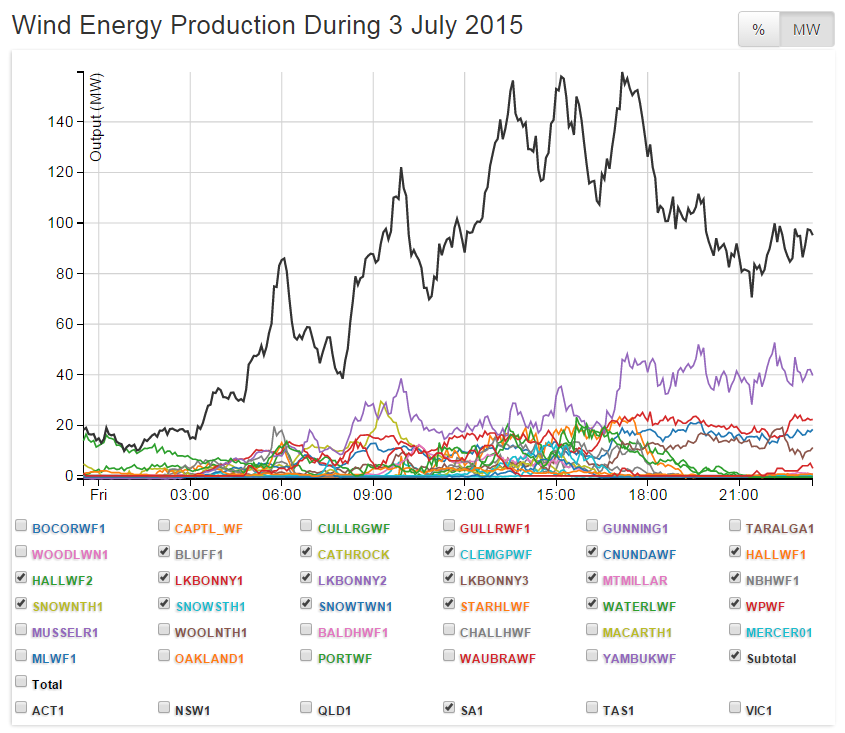

Electricity Pricing Event Report – Friday 03 July 2015

Market Outcomes: South Australian spot price reached $2,296.32/MWh for trading interval (TI) ending 0830 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached $13,333.95/MWh in South Australia for dispatch interval (DI) ending 0810 hrs. The high price can be attributed to a steep supply curve of generation capacity offered during morning peak demand period when wind generation was low in South Australia.

The South Australian demand was 1,990 MW for TI ending 0830 hrs. The high morning peak demand was due to the cool weather in Adelaide, with a low temperature of 3.5 °C at 0800 hrs gradually rising to 6.5°C at 0900 hrs at Adelaide Airport. During the high priced TI, wind generation in South Australia was low at 45 MW for TI ending 0830 hrs.

For DI ending 0810 hrs, South Australian generation capacity was offered at less than $590/MWh or above $10,750/MWh resulting in a steep supply curve. Cheaper priced generation were restricted by a fast-start unit (Hallett PS) which required time to synchronise.

Generation offers at $13,333.95/MWh had to be cleared from Northern PS units to meet the demand for the DI.

The target flow on the Heywood interconnector was limited to 444 MW towards South Australia by the binding thermal constraint equation, V>S_NIL_HYTX_HYTX. This system normal thermal constraint equation manages post contingent flow on the Heywood 275/500 kV transformers by reducing Heywood interconnector flow when the actual flow exceeds the pre-defined transformer rating. The target flow on the Murraylink interconnector was limited to 179 MW towards South Australia by a voltage stability constraint equation, V^SML_NSWRB_2. This constraint equation avoids voltage collapse in Victoria for loss of the Darlington Point to Buronga (X5) 220 kV line.

The 5-minute price reduced to $103.93/MWh in the subsequent DI to the high priced interval. South Australia demand reduced by 96 MW when 105 MW of non-scheduled generation came online. Generation capacity was also rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as the forecast demand in pre-dispatch was lower. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

AEMO July 2015

****

Next time you’ve got some wind-worshipper or wind industry parasite claiming that wind power lowers power prices, flick them a link to this post and ask them to explain – if they can? – how a wholly weather dependent power generation source lowers power prices when the wind drops to a zephyr?

When wind power output completely disappears – as it does almost every day – spot prices head north at rates slicker than anything set by Australian Formula One Ace, Mark Webber.

A whole shadow industry has been developed around wind power ‘outages’.

****

In the reports above, you’ll see references to the “fast-start unit (Hallett Power Station)”; “fast-start unit (Dry Creek GT)”; “Mintaro GT and “Quarantine PS”. Each of these “fast-start units” use Open Cycle Gas Turbines (OCGTs) – which are little more that jet engines, run on gas or fuel oil (diesel) or kerosene.

The initial capital outlay is low, but their operating costs are exorbitant – depending on the fuel input costs (the gas dispatch price varies with demand, for example) operators need to recoup upwards of $300-400 per MWh before they will even contemplate firing them into action. For a wrap up on “fast-start-peakers” see this paper: Peaker-Case-Histories

As to the insane cost of running them, see this article: OPEN GAS CYCLE TURBINES: Between a rock and a hard place

For peaking power operators, the inevitable and total collapses in wind power output is where the greatest rort of all time begins.

You see, it’s not really about the costs of running OCGTs (or diesel engined generators) this is all about what the operator can get away with.

The pattern was set up by the energy market whizzkids from Enron – back in the days when it raped and pillaged the Californian power market, using much the same tactics. Wait for an “outage” – self-generated in Enron’s case – sit back and watch the grid manager panic about widespread blackouts; and then ‘offer’ to solve the problem by delivering power in the nick of time at rates 1000 times the average price: the Enron rort was detailed in the doco “The Smartest Guys in the Room”.

***

***

For the purchaser (grid manager), it’s not about how much the vendor ‘needs’ to cover its costs – it’s all about how much the grid manager has ‘got’: some might call it ‘chiselling’; others ‘naked theft’. Hence, the NEM rules that set the upper limit of what can be charged at $13,800 per MWh.

However, there is a serious move to increase the cap to …. be sure you’re seated for this … $80,000 per MWh. See this paper by Dr Jenny Riesz here: Energy-only markets with high renewables: Can they work?

For a ‘wishy-washy’ analysis on the debacle above, note the excuses from wind power fans, Watt-Clarity, here: Why large energy users are concerned about last week’s machinations in South Australia

The ‘alternative’ to increasing the mandatory price cap from its already whopping $13,800 per MWh to a phenomenal $80,000, is to pay baseload generators $millions upfront to hold additional spinning reserve – with plants permanently ready to come online to cover wind power collapses; and, therefore, burning coal and gas around the clock – with what are called “capacity payments”:

All of this power market insanity is the direct consequence of inevitable but unpredictable wind power output collapses; the criminal scenarios detailed above will only get worse if young Gregory Hunt’s ultimate annual 33,000 LRET were ever met; and would become a complete social and economic disaster if Labor’s 50% renewable target fantasy were ever realised.

One way or another – whether it’s the daily spot price “bonanza” enjoyed by peaking-power-piranhas; or paying millions of dollars in capacity payments to baseload generators, just to keep the grid from collapsing when the wind stops blowing – it’s power punters that pay the ultimate price. And, for South Australians, the only way is up.

Once upon a time, South Australia enjoyed the cheapest power prices in the world; and, with it, an unparalleled burst of economic growth and prosperity:

ETSA: Sir Tom Playford’s Ghost

Today, however, thanks to the most ludicrous power ‘policy’ in the Nation, it’s an economic train wreck. And they wonder why?

Then simply follow South Australia’s wind power ‘policy’.

Some thoughts from a friend who until recently worked at Eraring Energy:

There are some issues that require comment.

A substantial degree of wind generation receives the pool price no matter what. There is grandfathered generation which was registered before new rules were put in place wind generators which require bidding. However, It is unlikely that SA will get much more wind capacity in place as it is almost running out of wind sites.

The fact that there are high prices in South Australia is that the Heywood and Murraylink interconnector have limited capacity to transfer energy from both Victoria and New South Wales. These interconnectors are in effect “ quasi generators”. When there are transmission constraints in Victoria, the interconnectors become partially or fully binding and no further generation can pass into South Australia.

In the past, augmentations of both links have been reviewed but cannot be justified on their economic merit. This, in part, is due to the transmission losses of around 20%.

Rebidding by the South Australian participants is lawful and was part of the market design. It is not illegal after a legal challenge by the AER.

Anyway, if prices were to go up as a result of strategic rebidding, wouldn’t new capacity be developed? Just recall that the Northern Power Station has recently been closed as it had reached the end of its useful life. Even higher prices could not justify its life extension.

South Australia’s problem is that it is at the end of the grid. You don’t see the high prices in the eastern leg of the NEM due to the highly messed transmission system. Prices in NSW/VIC/Snowy and Qld rarely divert.

This guy should be worried more about the very high community subsidies which will be given to renewable through the tax system which will total around $20Bn as I recall. This is borne by all taxpayers, and not just those in SA.

Another point is that there is a comment that an alternative to prevent the mandatory price cap from the current market cap to a a hypothetical $80,000 – based on the Reisz paper – is to pay baseload generators $millions upfront to hold additional spinning reserve. However, all of the coal-generators maintain generation minimums of their own – in Eraring’s case this is about 250 MW roughly per unit. Eraring will increase its generation if there is a fall in demand to maintain system frequency. It is built into the design of the generators and cannot be altered

Thanks Frank.

One question for you, if SA’s 1,477MW of installed wind power capacity were, instead, ‘dispatchable’ (ie available on demand) would the 8 extreme ‘pricing events’ evidenced for July have occurred? (anticipated answer ‘NO’).

Dr Riesz’s paper was directed at further increased capacity from non-dispatchable sources, ie wind and solar and the need to compensate base-load generators to invest (or remain in the market) to deal with low spot prices when the wind is blowing and remain profitable over the long-run.

Capacity payments are used in Europe – Germany, the UK etc for the same reasons discussed in her presentation:

And such payments are the only alternative to allowing an increase in the price gouging seen above. You say it’s ‘lawful’, but that doesn’t make it economically (or morally or politically) sustainable – with its power costs, SA already has some 50,000 homes without power because they can’t afford it anymore. Try justifying what’s detailed above to 50,000 SA families sitting freezing in the dark. The average spot price in SA (currently at $72) is fully double Victoria’s at $35. Wind power collapses and extreme pricing events go some way to explaining that.

We agree that the LRET cost is substantial, we have covered the topic many times:

But the routine natural and total ‘outages’ of wind power output are causing the extreme pricing events seen above (and recorded on hundreds of previous occasions) – there is no other way to read the evidence. The parallels with Enron’s (more deliberate) strategy in California – see the video – are obvious to Blind Freddy.

Once upon a time no-one had heard of OCGTs and none were needed to supply power, apart from remote locations: mines, say. Now they are everywhere and form an essential part of the Eastern grid. That is a ridiculous situation that would not exist without the need to back up the 3,669MW of wind power capacity that fails to deliver every other day.

I’ve done a quick read-through analysis and just by an understanding of this there is nothing more to assess and understand than that this is a major conspiracy against the energy consumers of this state, in particular and consumers Australia and world wide.

How on earth Premier Weatherill can bang on about renewables, aka windmills, and our state being the leaders, whilst being an imagined, gloating world leader in the same sentence, and hold a straight face is nothing less than farcical

When will these idiots be held to account?

When will the advisers of Premier Weatherill and planning minister John Rau place this information in front of them and explain to them that the reality of their support of the wind industry is much the same as one would explain to a 4 year old that it is pointless holding your breath in the pursuit of achieving the unwinnable?

There is only one thing that a person such as myself can ascertain, and that is the wind industry is nothing more or less than a conspiracy, with the aid of compliant governments, their departments and their hangers-on.

To hell with them all.

Essentially industrial wind turbines achievements are symbolic, and have no beneficial use, except to the bank balances of the wind weasels.

Time for the world to focus on renewables that do more good than harm, not these false flailing gods of the Green ecofascists.

Are not some of the ‘peaking power pirhana’s’ also major operators of wind factories?

It is therefore in their interests to build more intermittent wind and capitilise on the grid chaos.

Meanwhile the publicly intellectually interrupted like Dangerous Dave ‘Vader’ from Crystal Brook in South Australia cheer on in ignorant bliss.

And the trend continues into August. It will never end because the wind cannot be controlled to blow when they want it at the at the level they need and without its natural process of rising and falling in intensity constantly.

We in SA are constantly told wind will provide for our needs and if it can’t we will be supplied from Victoria’s coal production, well as seen above there are many times there is constraint on what they send us because of things like scheduled maintenance – which being scheduled cannot take into account how the wind will perform in SA.

Then of course what will happen when Victoria starts to shut down or reduce production from its coal and gas powered plants, will we be assured of a constant immediate back-up? Of course not they will keep what they need for themselves, and as has been the case recently across the Eastern Grid the wind does not necessarily have to be blowing across the whole Grid, at times wind has failed in each State at the same time.

Of course we don’t have to worry do we? As our Premier can work miracles can’t he?!