***

In Australia’s so-called wind power capital, South Australia, its hapless Labor government is crowing about having reached its ludicrous 50% renewable energy target. However, the cost of that vanity project is crippling what remains of South Australia’s productive enterprise.

In our recent post – Economic Carnage: SA’s Rocketing Power Prices Crippling Miners, Bakers & Brewers Alike – we covered the pain being felt by miners like BHP Billiton, bakers and brewers like South Australian icon, Coopers.

Now, South Australia’s butchers have joined the growing list of businesses reeling from power prices that just keep on doubling, almost every year. We deal with the reasons for South Australia’s rocketing power prices below, but first here’s The Australian’s Michael Owen.

South Australia’s ‘energy mess’ threatens to butcher jobs

The Australian

Michael Owen

11 April 2017

A 112-year-old butchers’ co-operative that directly employs more than 130 people in South Australia is facing financial ruin because of the state’s soaring energy prices.

As the Weatherill government yesterday celebrated achieving its 50 per cent renewable energy target almost eight years ahead of schedule, the food service business said it was the latest to face potential closure because of an “energy mess” created by the government.

Master Butchers Co-operative (MBL) has seen skyrocketing prices for electricity and gas blow out its energy costs by several million dollars a year. MBL chief executive Warren McLean, in a circular to members, said despite “rigorously looking” for better electricity and gas contracts, the “huge energy costs will severely impact on your co-op’s bottom line”.

Mr McLean said MBL had “reluctantly” agreed to a new electricity contract with a price rise of about $750,000 a year.

Since 2010, MBL’s electricity costs have increased by up to 448 per cent over the inflation rate of 13.5 per cent, he said.

“A new gas contract is currently being negotiated, with MBL facing a price rise of between double and triple the existing contract — a slug of between $1.2 million and $2.4m a year,” Mr McLean said. “Our current gas contract runs out at the end of December and we are looking at all options to address the threat to MBL.”

He told The Australian the increases in energy costs will “more than wipe out our annual profit for the last two years”. “It takes you from being a solid organisation to one that is unviable. Literally, with these price increases we will be unviable,” Mr McLean said.

Most of MBL’s energy use is at its Wingfield and Keith rendering plants, where the proteins division recycles about 140,000 tonnes of food industry waste that cannot be used in landfill, into export products. As tallow and meal are commodity-priced products, MBL cannot raise its prices to cover increasing production costs.

“While the electricity price is a major concern, a massive issue is a gas shortage which will keep driving up prices,” Mr Warren said.

“Only two companies have been willing to give us quotes for gas — others can’t buy enough gas to supply us because so much is being exported to Asia.”

MBL recently invested $8m in new processing equipment to cater for demand from poultry and pork industries. Mr McLean said MBL was the only service processor in South Australia and if it was forced to close “the product would be transported to Victoria along with the jobs”.

“SA’s electricity problem is down to the Weatherill government’s ridiculous commitment to renewable energy,” he said.

Mr McLean said the co-op approached the state government, only to be told to do an energy savings audit. “Their suggestion is ridiculous. We have just spent $480,000 on boiler efficiency upgrades. No further contact or follow up has been received,” he said.

SA Energy Minister Tom Koutsantonis said he was “very pleased” the state was “leading the nation” on renewables.

The Australian

Nation in unemployment & insolvencies.

***

South Australians must wake every morning and wonder what mortal sin was committed that sees them punished every day by a group of morally bankrupt idiots, who haven’t the faintest clue on energy and economics. No wonder dozens of businesses are planning to pack their bags and head over the border to Victoria, where power prices are a fraction of those in SA (thanks an abundance of reliable and cheap coal-fired power).

Now, let’s take a look at why South Australia’s power generation costs are close to triple those in Victoria. The figures we run below date back to 2015, which does not affect the substance or conclusion of our analysis: chaotic wind power costs.

What SA Pays when the Wind is Blowing

The villain behind the wind power disaster playing out in SA is the Federal Large-Scale Renewable Energy Target (LRET), which the Coalition government knows is doomed, but can’t bring themselves to say so out loud (see our post here).

As to how the LRET has wrecked SA’s power market, we’ll start with an observation by the Australian Financial Review’s Mark Lawson about how SA’s wind power outfits operate under the LRET:

When the wind is blowing strongly wind farm power will flood the market to pull prices down to minus $20 (generators pay retailers to take the power). This is obviously uneconomic for conventional generators, but wind and solar generators can still make some money under the renewable energy target.

In short, wind power outfits collect the same amount of revenue, irrespective of the spot price. However, conventional generators receive the prevailing price – and, unlike wind power outfits, do not receive any form of subsidy for what they dispatch: the market perversion driven by the LRET and subsidies for wind power is what has caused SA’s conventional generators to become unprofitable; and it’s that lack of profitability that led to Alinta’s decision to close its Northern Port Augusta plant in May last year.

The Power Purchase Agreements (PPAs) struck between wind power outfits and retailers (which you’ll never once see the likes of Infigen or Trustpower talk about publicly) are built around the massive stream of subsidies established by the Large-Scale Renewable Energy Target (LRET) – which is directed to wind power generators in the form of Renewable Energy Certificates (RECs aka LGCs).

Under PPAs, the prices set guarantee a return to the generator of between $90 to $120 per MWh for every MWh delivered to the grid.

In a 2014 company report, AGL (in its capacity as a wind power retailer) complained about the fact that it is bound to pay $112 per MWh under PPAs with wind power generators: these PPAs run for at least 15 years and many run for 25 years.

Wind power generators can and do (happily) dispatch power to the grid at prices approaching zero – when the wind is blowing and wind power output is high; at night-time, when demand is low, wind power generators will even pay the grid manager to take their power (ie the dispatch price becomes negative)(see our post here). As noted in the quote from the AFR, wind power outfits have been paying the grid operator up to $20 per MWh to take power with no commercial value.

However, the retailer still pays the wind power generator the same guaranteed price under their PPA – irrespective of the dispatch price: in AGL’s case, $112 per MWh.

PPA prices are 3-4 times the cost that retailers pay to conventional generators; retailers can purchase coal-fired power from Victoria’s Latrobe Valley for around $25-35 per MWh. Although with the closure of Hazelwood (and the loss of 1,600MW of base-load capacity), that cost has already jumped 20% and is bound to rise further.

Underlying the PPA is the value of the RECs (aka LGCs) that are issued to wind power generators and handed to retailers as part of the deal.

The issue and transfer of RECs under the LRET sets up the greatest government mandated wealth transfer seen in Australian history: the LRET is – without a shadow of a doubt – the largest industry subsidy scheme in the history of the Commonwealth. That transfer – which comes at the expense of the poorest and most vulnerable; struggling businesses; and cash-strapped families – is effected by the issue, sale and surrender of RECs. As Origin Energy chief executive Grant King correctly puts it:

“[T]he subsidy is the REC, and the REC certificate is acquitted at the retail level and is included in the retail price of electricity”.

It’s power consumers that get lumped with the “retail price of electricity” and, therefore, the cost of the REC Subsidy paid to wind power outfits. The REC Tax/Subsidy has already added over $10 billion to Australian power bills, so far.

Between 2017 and 2031, the mandatory LRET requires power consumers to pay the cost of issuing 450 million RECs to wind power generators. With the REC price currently $83 – and tipped to exceed $90 as retailers get hit with the shortfall penalty set by the LRET – the wealth transfer from power consumers to the Federal Government (as retailer penalties) and/or to the wind industry (as REC Subsidy) will be somewhere between $40 billion and $50 billion, over the next 15 years: It’s Time for Frydenberg & Turnbull to Come Clean on the Cost of Subsidised Wind Power

With more wind power capacity per head than any other State, South Australians are going to be lumbered with a disproportionate share of the ludicrous cost of the REC Tax/Subsidy, set by the LRET.

A cost that is already forcing major employers like Nyrstar to consider shutting up shop – with the immediate loss of 750 jobs in economically depressed Port Pirie. And more than 50,000 SA homes to do without any power at all, now (see our post here). And, which is one half of the reason why South Australians are being belted with power price increases that are 4-5 times the rate of inflation. Here’s the other half.

What SA Pays when the Wind Stops Blowing

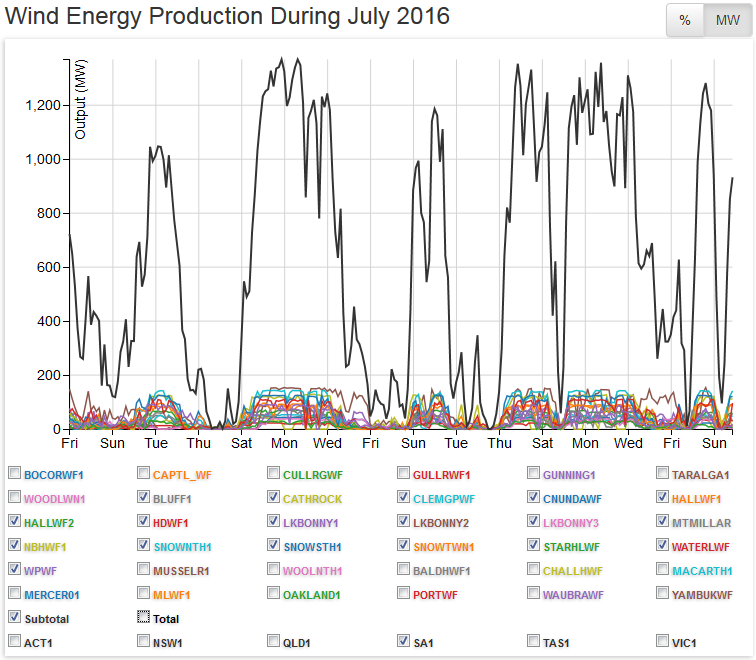

SA is lumbered with 18 wind farms, with a ‘notional’ installed capacity of 1,576MW – it has the greatest number of turbines per capita of all States – and the highest proportion of its generating capacity in wind power by a country mile.

The chaos that wind power brings with it, has created the perfect opportunity for peaking power operators (running highly inefficient Open Cycle Gas Turbines and diesel generators) to make out like bandits at power consumers’ expense – simply because it can be predictably ‘relied’ on to disappear without warning (see above).

Wind power driven, market chaos clearly has the Australian Energy Market Operator worried; and, if SA’s journalists were on the ball, should have policy makers anxious and voters/power consumers furious.

To detail what we mean we’ll pick up on an AEMO analysis of SA’s spot market. The following comes from AEMO’s ‘Pricing Event Report’ for SA for July 2015. To which we’ve added daily output data, care of Aneroid Energy.

In 2015, SA’s average spot price for power was running around $72 per MWh (compared to Victoria’s $35). The reason for the price difference has a lot to do with the fact that the Victorians have a relatively tiny proportion of their generating capacity in wind power; and the largest coal-fired generators in the country.

Now, with SA’s 2015 average of $72 per MWh in mind, consider the number of occasions in July when – as wind power output collapses – the spot price approaches or hits the Market Price Cap. That cap – currently $14,000 per MWh and $13,800 per MWh in 2015 – sets the upper limit of what peaking power generators can extort from the system: for a rundown on how the National Energy Market is designed to work, see this paper: AEMO Fact Sheet National Electricity Market

That’s the ‘design’; here’s the shocking reality.

Pricing Event Reports – July 2015

Electricity Pricing Event Report – Tuesday 28 July 2015 (TI ending 1830 hrs)

Market Outcomes: South Australian spot price reached $1,967.51/MWh for trading interval (TI) ending 1830 hrs.

South Australian FCAS prices (Volume Weighted FCAS Prices) and energy and FCAS prices for the other NEM regions were not affected by this event.

South Australia had an actual Lack of Reserve 1 (LOR1) from 1800 hrs to 2030 hrs (Market Notices 49437 and 49438).

Detailed Analysis: 5-Minute dispatch price reached $10,759.20/MWh for dispatch interval (DI) ending 1820 hrs. The high price can be attributed to rebidding of generation capacity and limited interconnector flows during the evening peak demand period. Wind generation was low during this period in South Australia.

The South Australian demand was 2,233 MW for TI ending 1830 hrs. During the same TI, wind generation in South Australia was at 18 MW.

For DI ending 1820 hrs, a total of 38 MW of generation capacity was rebid from Hallett PS and Northern PS unit 2 from bands priced at or below $590.07/MWh to bands priced above $13,333/MWh. South Australian generation capacity was offered at less than $591/MWh or above $10,759/MWh resulting in a steep supply curve.

Cheaper priced generation were restricted by their ramp rates (Mintaro GT) and FCAS profiles (Torrens Island A units 3 and 4). Generation offers at $10,759.20/MWh had to be cleared from Dry Creek GT unit 3 to meet the demand for the DI.

During the affected DI, the target flow towards South Australia on the Heywood interconnector was constrained to 403 MW by an outage constraint equation V::S_XKHTB1+2_MAXG. This transient stability constraint equation manages the Victoria to South Australia flow for the loss of the largest generation block in South Australia during the outage of both parallel Keith – Tailem Bend 132 kV lines.

The target flow on the Murraylink interconnector was limited to 68 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $104.27/MWh in the subsequent DI to the high priced interval when 673 MW of generation capacity was rebid from higher priced bands to the market floor price of -$1,000/MWh.

The high 30-minute spot price for South Australia was forecast in pre-dispatch schedules prior to TI ending 1130 hrs. The pre-dispatch schedule for TI ending 1830 hrs forecast a spot price of $590.07/MWh. The difference in prices between Pre-dispatch and Dispatch was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices.

Electricity Pricing Event Report – Tuesday 28 July 2015

Market Outcomes: South Australian spot price reached $2,390.06/MWh for trading interval (TI) ending 0800 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached the Market Price Cap (MPC) of $13,800/MWh in South Australia for dispatch interval (DI) ending 0750 hrs. The high price can be attributed to rebidding of generation capacity resulting in a steep supply curve during the morning peak demand period. Wind generation was low during this period in South Australia.

The South Australian demand was 1,915 MW for TI ending 0800 hrs. During the high priced TI, wind generation in South Australia was at 19 MW.

For DI ending 0750 hrs, AGL shifted a generation capacity of 160 MW from Torrens Island B PS from bands priced at or below $124.99/MWh to bands priced at MPC of $13,800/MWh. South Australian generation capacity was offered at less than $591/MWh or above $12,195/MWh resulting in a steep supply curve.

Cheaper priced generation were restricted by their ramp rates (Hallett PS, Mintaro GT, Quarantine PS unit 4) and fast-start profiles (Dry Creek GT unit 3) which required time to synchronise.

Generation offers at Market Price Cap (MPC) of $13,800/MWh had to be cleared from Torrens Island B PS to meet the demand for the DI.

During the affected DI, the target flow towards South Australia on the Heywood interconnector was constrained to 460 MW by the Victoria to South Australia Heywood upper transfer limit thermal constraint equation, V>S_460. The target flow on the Murraylink interconnector was limited to 61 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $109.32/MWh in the subsequent DI to the high priced interval when South Australia demand reduced by 77 MW. Approximately 101 MW of non-scheduled generation came online. Generation capacity was also rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

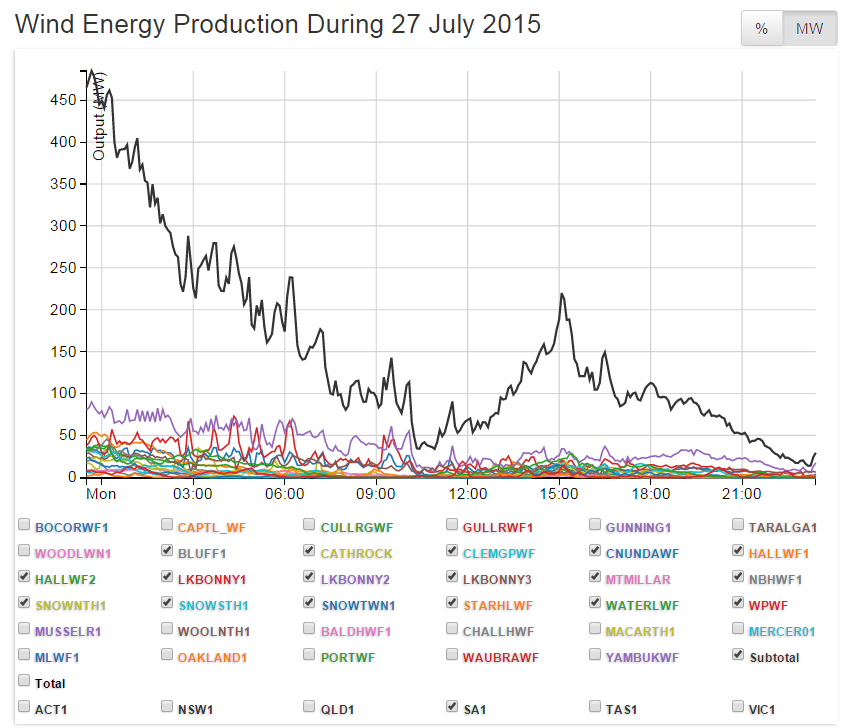

Electricity Pricing Event Report – Monday 27 July 2015

Market Outcomes: South Australian spot price reached $4,449.17/MWh for trading interval (TI) ending 0800 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached the Market Price Cap (MPC) of $13,800/MWh and $12,195.07/MWh in South Australia for dispatch intervals (DIs) ending 0755 hrs and 0800 hrs respectively.

The high prices can be attributed to rebidding of generation capacity resulting in a steep supply curve during the morning peak demand period. Wind generation was moderately low during this period in South Australia.

The South Australian demand was 1,896 MW and the temperature in Adelaide was 4.9 °C for TI ending 0800 hrs. During the high priced TI, wind generation in South Australia was at 141 MW.

For DI ending 0755 hrs, AGL shifted a generation capacity of 200 MW from Torrens Island B PS from bands priced at or below $174.99/MWh to bands priced at MPC setting the high price. South Australian generation capacity was offered at less than $591/MWh or above $10,759/MWh resulting in a steep supply curve.

Cheaper priced generation were restricted by their ramp rates (Hallett PS), FCAS profiles (Northern PS unit 2) and fast-start profiles (Dry Creek GT units 2 and 3) which required time to synchronise.

For DI ending 0800 hrs, cheaper priced generation were restricted by fast-start profiles (Dry Creek GT units 2 and 3) which required time to synchronise. Generation offers at $12,195.07/MWh had to be cleared from Hallett PS to meet the demand for the DI.

During the high priced DIs, the target flow on the Heywood interconnector was limited up to 418 MW towards South Australia by the binding transient stability constraint equations, V::S_NIL_MAXG_SECP and V::S_NIL_MAXG_AUTO. The V::S_NIL_MAXG_SECP constraint equation prevents transient instability by limiting flow on the Heywood interconnector from Victoria to South Australia for the loss of the largest generator in South Australia for periods when the South East capacitor is unavailable for switching. The V::S_NIL_MAXG_AUTO constraint equation prevents transient instability by limiting flow on the Heywood interconnector from Victoria to South Australia for the loss of the largest generation block in South Australia.

The target flow on the Murraylink interconnector was limited to 58 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $174.99/MWh in the subsequent DI to the high priced interval when generation capacity from several South Australian generators were shifted to lower priced bands.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

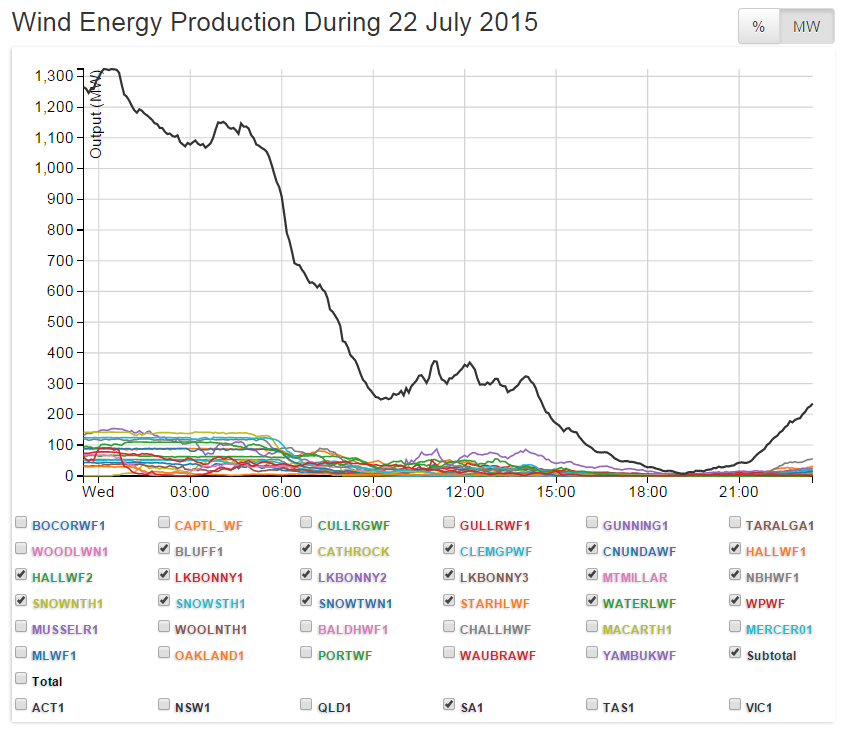

Electricity Pricing Event Report – Wednesday 22 July 2015

Market Outcomes: South Australian spot price reached $2,296.07/MWh for trading interval (TI) ending 1830 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached $13,481.81/MWh in South Australia for dispatch interval (DI) ending 1810 hrs. The high price can be attributed to a steep supply curve of generation capacity offered during evening peak demand period when wind generation was low in South Australia.

The South Australian demand was 2,100 MW for TI ending 1830 hrs. During the high priced TI, wind generation in South Australia was low at 39 MW.

For DI ending 1805 hrs, Energy Australia shifted a generation capacity of 34 MW from Hallett PS from bands priced at $360.81/MWh to bands priced at $13,481.81/MWh. For DI ending 1810 hrs, AGL rebid a generation capacity of 100 MW from Torrens Island B PS from bands priced at or less $64.99/MWh to bands priced at $13,500/MWh. South Australian generation capacity was offered at less than $591/MWh or above $10,750/MWh resulting in a steep supply curve. Cheaper priced generation was restricted by FCAS profiles (Northern PS unit 2 and Torrens Island PS unit A4) and fast-start units (Mintaro PS and Quarantine PS) which required time to synchronise.

Generation offers at $13,481.81/MWh had to be cleared from Hallett PS to meet the demand for the DI.

The target flow on the Heywood interconnector was limited to 447 MW towards South Australia by the binding transient stability constraint equation, V::S_NIL_MAXG_AUTO. This constraint equation prevents transient instability by limiting flow on the Heywood interconnector from Victoria to South Australia for the loss of the largest generation block in South Australia. The target flow on the Murraylink interconnector was limited to 64 MW towards South Australia by the outage constraint equation, V>X_NWCB6022+6023_T1.

This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the Monash – North West Bend No. 2 132 kV line from 22 July 2015.

The 5-minute price reduced to $53.42/MWh in the subsequent DI to the high priced interval. South Australia demand reduced by 103 MW when 101 MW of non-scheduled generation came online. Generation capacity was also rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of rebidding of generation capacity within the affected trading interval. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

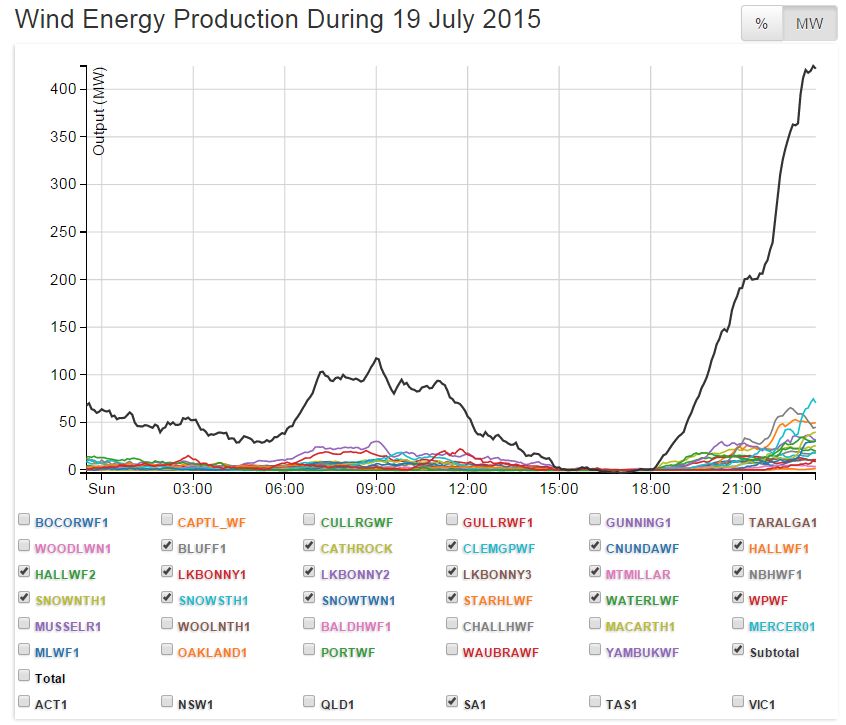

Electricity Pricing Event Report – Sunday 19 July 2015

Market Outcomes: South Australian spot price reached $2,372.11/MWh for trading interval (TI) ending 1830 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price in South Australia reached $13,333.95/MWh for dispatch interval (DI) ending 1830 hrs. The high price can be attributed to a steep supply curve in generation capacity during the evening peak demand period when wind generation was low in South Australia.

The South Australian demand was 2,066 MW for TI ending 1830 hrs. The high evening peak demand was due to the cool weather in Adelaide, with a low temperature of 7.3°C at 1830 hrs. During the high priced TI, wind generation in South Australia was low at 3 MW for TI ending 1830 hrs.

For DI ending 1825 hrs, Alinta Energy rebid 95 MW of Northern PS generation capacity from bands priced at or less than $286.95/MWh to $13,333.95/MWh. South Australian generation capacity was offered at less than $591/MWh or above $10,750/MWh resulting in a steep supply curve for the high priced DI. Cheaper priced generation were restricted by ramp rates (Torrens Island Unit A4), FCAS profiles (Northern PS Unit 2) or required time to synchronise (Hallett PS).

Generation offers at $13,333.95/MWh had to be cleared from Northern PS units to meet the demand for the DI.

The target flow on the Heywood interconnector was limited to 448 MW towards South Australia by the thermal constraint equation, V>S_NIL_HYTX_HYTX. This system normal thermal constraint equation manages post contingent flow on the Heywood 500/275 kV transformers by reducing Heywood interconnector flow when the actual flow exceeds the pre-defined transformer rating. The target flow on the Murraylink interconnector was limited to 64 MW towards South Australia by the outage constraint equation, V>X_NWCB6225+6021_T1. This constraint equation limits flow from Victoria to South Australia on Murraylink during the planned outage of the North West Bend 132 kV circuit breakers from 13 July 2015.

The 5-minute price reduced to $115.77/MWh in the DI subsequent to the high priced interval when demand reduced by 111 MW and 101 MW of non-scheduled generation came online.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as the forecast demand in pre-dispatch was lower.

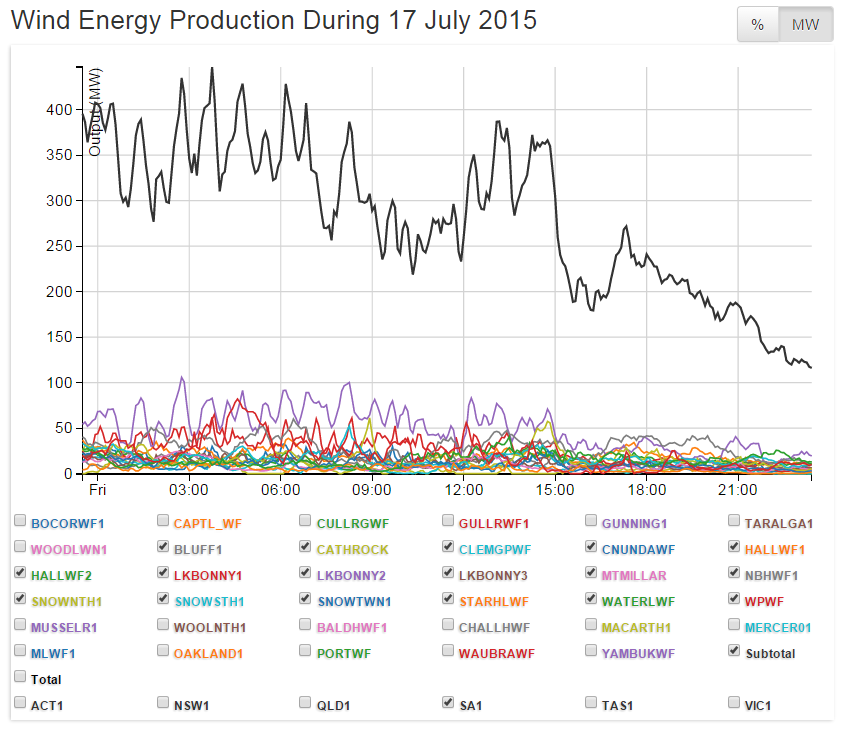

Electricity Pricing Event Report – Friday 17 July 2015 (TI ending 0000 hrs on 18 July 2015): South Australia

Market Outcomes: South Australian spot price reached $2,256.25/MWh for trading interval (TI) ending 0000 hrs (on Saturday, 18 July 2015).

FCAS prices and energy prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached $13,333.95/MWh in South Australia for dispatch interval (DI) ending 2340 hrs on 17 July 2015 during high demand period due to hot water load management (ripple control). Between DIs ending 2325 hrs and 2340 hrs, the South Australian demand increased by 311 MW. This additional load represented an 18% increase in the South Australian demand.

Wind generation in South Australia was approximately 120 MW for TI ending 0000 hrs on 18 July 2015.

At DI ending 2335 hrs, a total of 150 MW of generation capacity from Northern PS was shifted from bands priced at or less than $286.95/MWh to $13,333.95/MWh. The high price for DI ending 2340 hrs was set by Northern PS at $13,333.95/MWh. Cheaper priced generation was available from fast-start units (Hallet and Dry Creek unit 3) which required time to synchronise.

The target flow on the Heywood interconnector was limited to 449 MW towards South Australia by a thermal constraint equation, V>S_NIL_HYTX_HYTX for DI ending 2340 hrs. This system normal constraint equation manages post contingent flow on the Heywood 275/500 kV transformers by reducing the Heywood interconnector flow when the actual flow exceeds the pre-defined transformer rating. The target flow on the Murraylink interconnector was limited to 66 MW towards South Australia by an outage constraint equation, V>X_NWCB6225+6021_T1. This constraint equation manages limits flow from Victoria to South Australia on Murraylink during the planned outage of the North West Bend 132 kV circuit breakers from 13 July 2015.

The 5-minute price reduced to $47.13/MWh for the next interval (DI ending 2345 hrs) when the demand reduced by approximately 122 MW and 102 MW of non-scheduled generation came online. A total of 349 MW of generation capacity was also rebid from higher priced bands to the market floor price of -$1,000/MWh.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as it was a result of a 5-minute load increase that caused a price spike in the 5-minute dispatch prices.

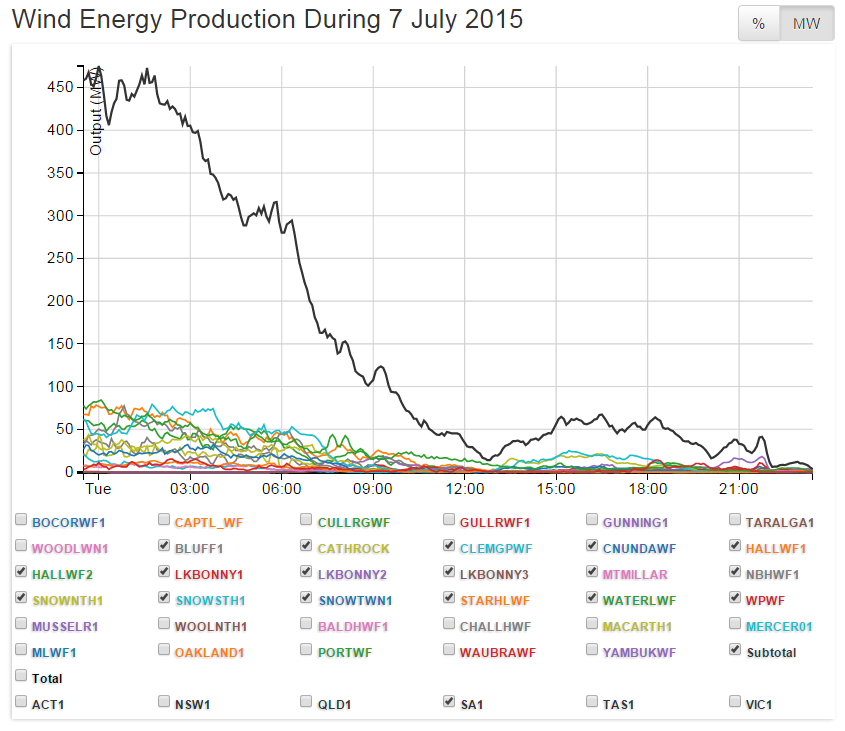

Electricity Pricing Event Summary – Tuesday 7 July 2015*

Market Outcomes: South Australia spot price reached $1,221.54/MWh for trading interval (TI) ending 1900 hrs. South Australia FCAS prices and energy and FCAS prices in other regions were not affected.

Summary:

South Australia 5-Minute dispatch price reached $6,794.04/MWh for dispatch interval (DI) ending 1855 hrs due to a steep supply curve in generation capacity during a period of low wind generation. Planned outages affecting the interconnector flow into South Australia also contributed to the high price.

- Low levels of wind generation in South Australia at approximately 60 MW at TI ending 1900 hrs

- Rebidding of 20 MW of Hallett PS generation capacity from bands priced at or less than $360.81/MWh to bands priced at $13,481.81/MWh for DI ending 1840 hrs

- For DI ending 1855 hrs, South Australian generation capacity was offered at less than $590/MWh or above $10,750/MWh resulting in a steep supply curve

- Cheaper priced generation were restricted by a fast-start unit (Dry Creek GT unit 3) which required time to synchronise

- The target flow on the Heywood interconnector was limited to 430 MW towards South Australia by a planned outage thermal constraint equation, V>S_APHY2_NIL_HYTX2. This constraint equation manages flow of the Heywood M2 transformer during the outage of APD-HYTS No. 2 500 kV line

- The target flow on the Murraylink interconnector was limited to 181 MW towards South Australia by a planned outage constraint equation, S>>RBTX1_RBTX2_WEWT. This constraint equation manages post contingent flow of Waterloo East – Waterloo 132 kV line for the trip of Robertstown No. 2 132/275 kV transformer during the outage of Robertstown No. 1 132/275 kV transformer.

South Australia energy price reduced to $46.14/MWh for DI ending 1900 hrs when:

- Demand reduced by 144 MW and 104 MW of non-scheduled generation came online

- Generation capacity was rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as the forecast demand in pre-dispatch was lower.

* A summary was prepared as the maximum daily spot price was between $500/MWh and $2,000/MWh

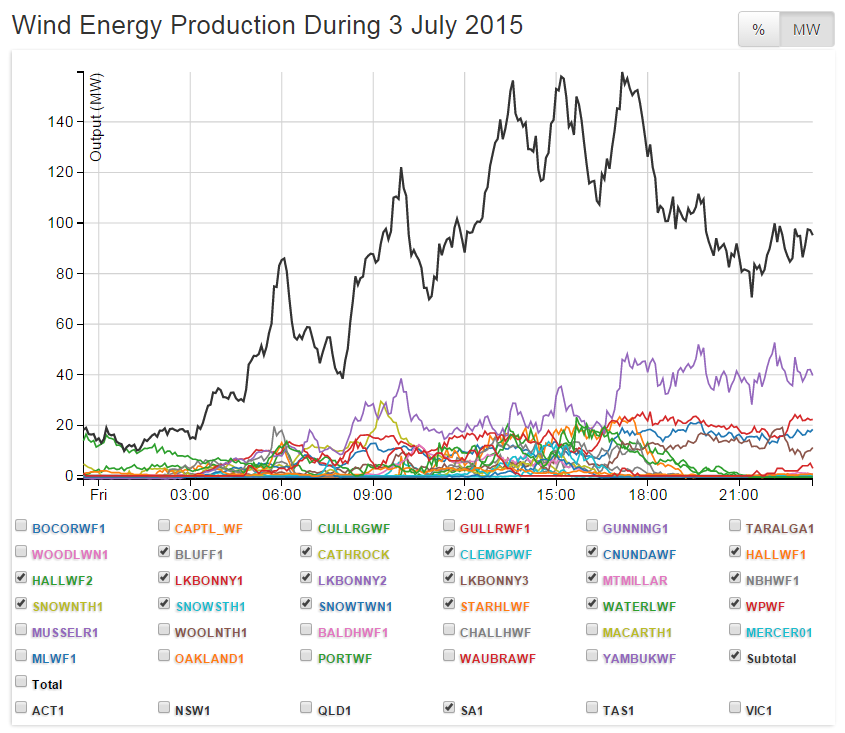

Electricity Pricing Event Report – Friday 03 July 2015

Market Outcomes: South Australian spot price reached $2,296.32/MWh for trading interval (TI) ending 0830 hrs.

South Australian FCAS prices and energy and FCAS prices for the other NEM regions were not affected by this event.

Detailed Analysis: 5-Minute dispatch price reached $13,333.95/MWh in South Australia for dispatch interval (DI) ending 0810 hrs. The high price can be attributed to a steep supply curve of generation capacity offered during morning peak demand period when wind generation was low in South Australia.

The South Australian demand was 1,990 MW for TI ending 0830 hrs. The high morning peak demand was due to the cool weather in Adelaide, with a low temperature of 3.5 °C at 0800 hrs gradually rising to 6.5°C at 0900 hrs at Adelaide Airport. During the high priced TI, wind generation in South Australia was low at 45 MW for TI ending 0830 hrs.

For DI ending 0810 hrs, South Australian generation capacity was offered at less than $590/MWh or above $10,750/MWh resulting in a steep supply curve. Cheaper priced generation were restricted by a fast-start unit (Hallett PS) which required time to synchronise.

Generation offers at $13,333.95/MWh had to be cleared from Northern PS units to meet the demand for the DI.

The target flow on the Heywood interconnector was limited to 444 MW towards South Australia by the binding thermal constraint equation, V>S_NIL_HYTX_HYTX. This system normal thermal constraint equation manages post contingent flow on the Heywood 275/500 kV transformers by reducing Heywood interconnector flow when the actual flow exceeds the pre-defined transformer rating. The target flow on the Murraylink interconnector was limited to 179 MW towards South Australia by a voltage stability constraint equation, V^SML_NSWRB_2. This constraint equation avoids voltage collapse in Victoria for loss of the Darlington Point to Buronga (X5) 220 kV line.

The 5-minute price reduced to $103.93/MWh in the subsequent DI to the high priced interval. South Australia demand reduced by 96 MW when 105 MW of non-scheduled generation came online. Generation capacity was also rebid from higher price bands to the market floor price of -$1000/MWh which also contributed to reducing the dispatch price.

The high 30-minute spot price for South Australia was not forecast in the pre-dispatch schedules, as the forecast demand in pre-dispatch was lower. The wind generation forecast for pre-dispatch was also marginally higher, which also contributed to the difference in prices between pre-dispatch and Dispatch.

AEMO July 2015

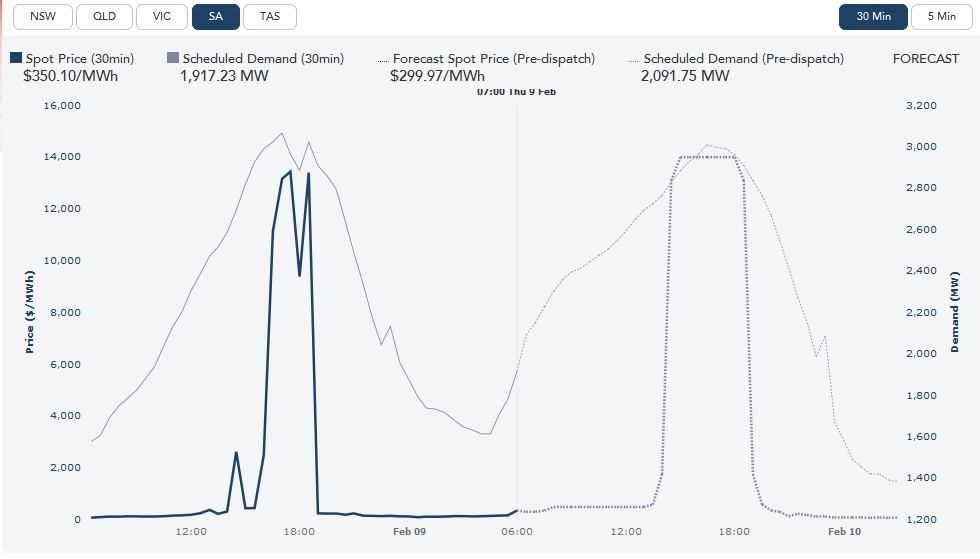

Since 2015, the chaotic market fundamentals haven’t changed. As just one recent example, as South Australians sweltered in 40°C heat on 8 February 2017 and wind power output collapsed by over 900 MW in a few short hours:

The spot price twice went from around $70 per MWh to $13,000 per MWh:

And the grid manager was forced to ‘load shed’, leaving 90,000 families boiling in the dark. From here, South Australians can expect a whole lot more of the same.

So, in a nutshell: South Australians are paying a minimum of around $110 per MWh for wind power when the wind is blowing (compared with the Victorian average spot price of around $54); and, when the wind stops blowing, are paying a spot price that quickly hits $2,000 per MWh and often hits the regulated market cap – currently $14,000 per MWh.

It’s an economic and social nightmare that any sane politician would be bursting to escape from. But, not in SA. Its Labor government, headed by the vapid Jay Weatherill only wants more of the same: crowing about reaching his 50% RET and only wanting more.

If anyone is unsure how a wind powered ‘future’ might look, then look no further than South Australia.

Load shedding and blackouts are the norm for all South Australians, but with power generation costs triple Victoria’s, tens of thousands are going to experience energy poverty of a kind that makes life a grinding misery: no electric light; no air-conditioning; no refrigeration – or, instead, going hungry in an attempt to afford a little of what were once reasonable expectations – reasonable even for low income earners and pensioners – which have quickly become tantalising luxuries for all too many.

And for business, it’s a case of get out before your creditors wipe you out.

Welcome to your wind powered future!

Reblogged this on ajmarciniak.

Hi,

I started a PETITION “SA PREMIER JAY WEATHERILL : Demand the RESIGNATION of the Energy Minister for HIGH POWER PRICES CAUSING SA’s JOBS CRISIS and 15,000 household POWER DISCONNECTIONS, frequent POWER BLACKOUTS and the JULY 2016 POWER CRISIS” and wanted to see if you could help by adding your name.

Our goal is to reach 200 signatures and we need more support.

You can read more and sign the petition here:

https://www.change.org/p/sa-premier-jay-weatherill-demand-the-resignation-of-the-energy-minister-for-high-power-prices-causing-sa-s-jobs-crisis-and-also-15-000-household-power-disconnections-frequent-power-blackouts-and-the-july-2016-power-crisis?recruiter=135406845&utm_source=share_petition&utm_medium=email&utm_campaign=share_email_responsive

Please share this petition with anyone you think may be interested in signing it.

Thankyou for your time.

Reblogged this on Climatism and commented:

Unreliable/Novelty/Feel-Good Energy Update :

“Load shedding and blackouts are the norm for all South Australians, but with power generation costs triple Victoria’s, tens of thousands are going to experience energy poverty of a kind that makes life a grinding misery: no electric light; no air-conditioning; no refrigeration – or, instead, going hungry in an attempt to afford a little of what were once reasonable expectations – reasonable even for low income earners and pensioners – which have quickly become tantalising luxuries for all too many.

And for business, it’s a case of get out before your creditors wipe you out.

Welcome to your wind powered future!”